Bold strategies and solutions are needed to win the technological race against scammers and cybercriminals.

Summary

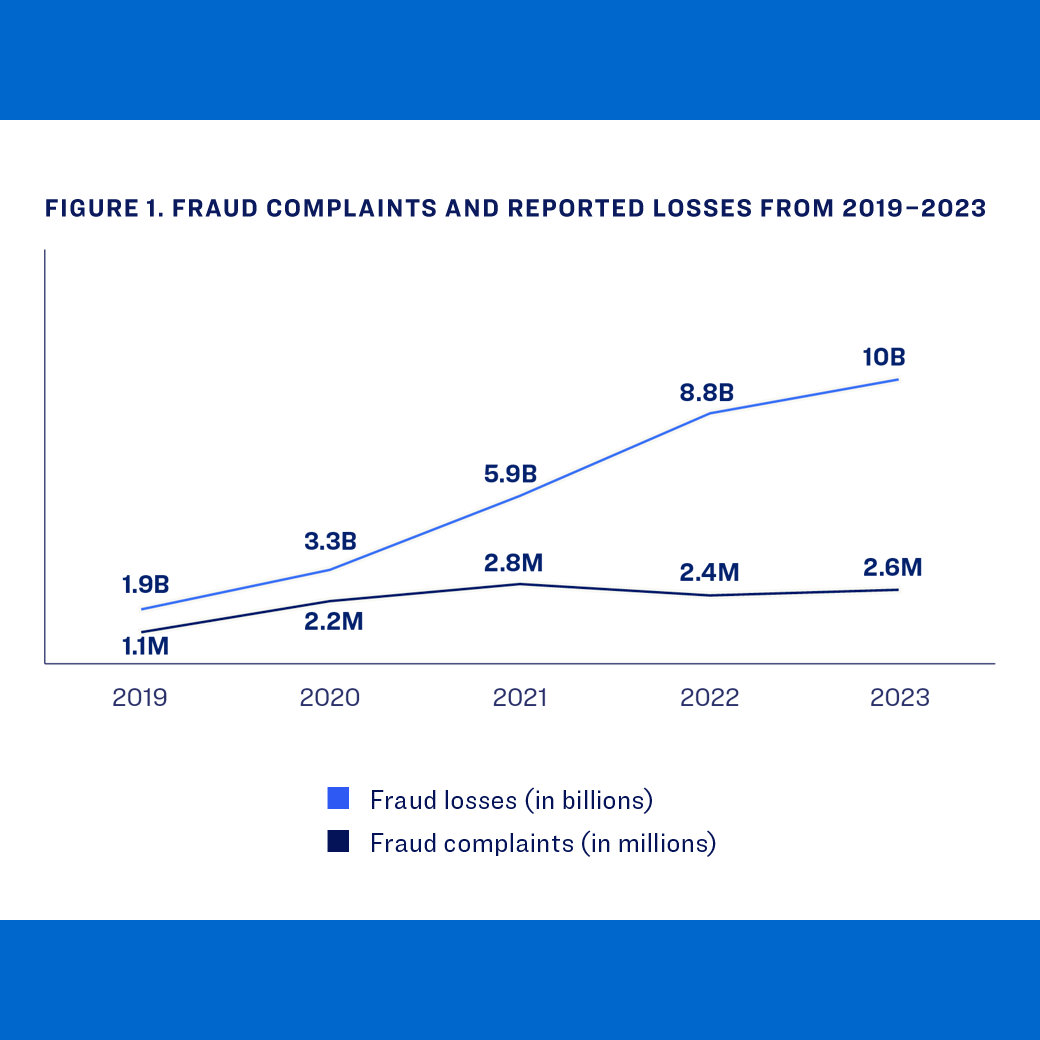

Millions of Americans each year are targeted by scams that use low-cost communication methods—such as email, text, social media and telephone calls—to steal money from prospective victims, jeopardizing their retirement security. Older adults experience a higher rate of victimization, but advances in artificial intelligence, telecommunications and cryptocurrencies have made it easier for scammers to target people of all ages with alarming speed and sophistication. This report examines the magnitude of fraud across the U.S. and what retirement plan providers, sponsors and participants can do to mitigate the problem.

Key Insights

- Although fraud is vastly underreported, older victims who file complaints typically report much higher median losses compared to younger victims—$1,450 for those age 80 or older compared to less than $500 for those ages 20 to 59.

- To reduce scam victimization, retirement plan providers can harness new technology to authenticate plan participants, secure their accounts, flag suspicious transactions, elevate awareness and advocate for increased protection.

- Plan sponsors can educate employees on ways to detect fraud and encourage adoption of account security features.

- Plan participants can educate themselves on the hallmarks of scams and add trusted contacts to their financial accounts.